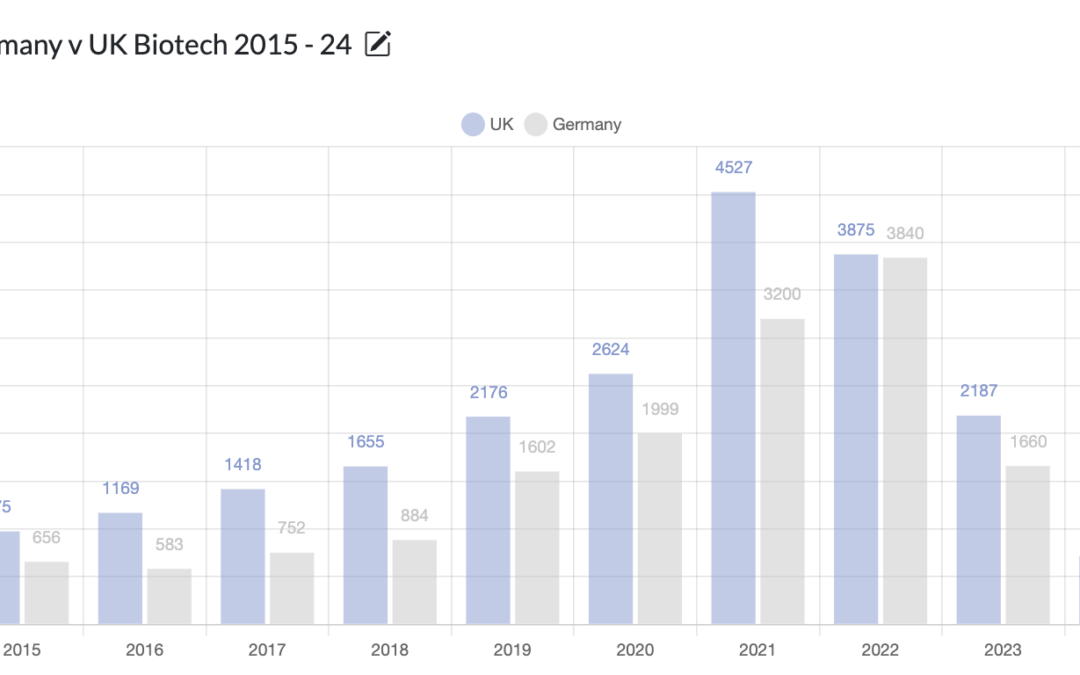

With the slump in the pharmaceutical sector set to continue, the long-awaited reforms to the MHRA have yet to materialise. As a result, drug approval in the UK lags behind the EU, further depressing the sector. 2023 seems to be the low point in that there has been an uptick in Q1 so far, and if this continues, it will increase by 9.1% this year compared to last. The recovery has been in London specifically, with volumes up 26.1% on last year.

If the worst kept secret in politics is that Kier Starmer will be the next Prime Minister, (the latest odds give him an 87% chance of being so) then upon taking power, he will have to make a decision about which Tory policies to continue, and which, to discard. No set of policies are more divisive than those to do with Brexit, hence spotlighting Biotechnology which is now starting to be negatively impacted, following the pandemic period ending and the industry globally returning to equilibrium, as this is an area that Starmer may need to change UK policy on, in order to revitalize.

Insurance companies face new risks due to economic volatility, higher interest rates, geopolitical uncertainty, and climate change. This has led to a rise in demand for risk professionals, with vacancies up by 11.4% in 2024 compared to last year. March 2024 had the highest number of risk vacancies in over a year, indicating a continuing trend.

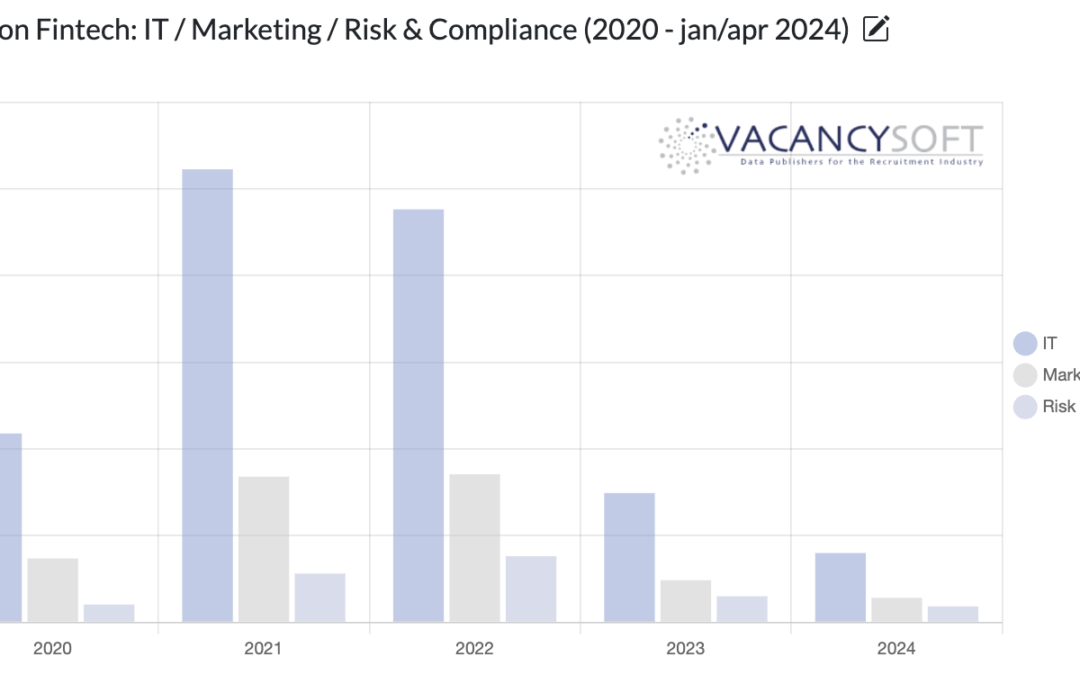

After a torrid 2023, the signs are positive for Fintech as VC funding into the sector accelerates. According to a recent report by Dealroom and HSBC, in Q1 of 2024, there were 73 rounds completed in Q1 of this year, totalling $1.4BN, making it the leading sector for investment, this year so far.

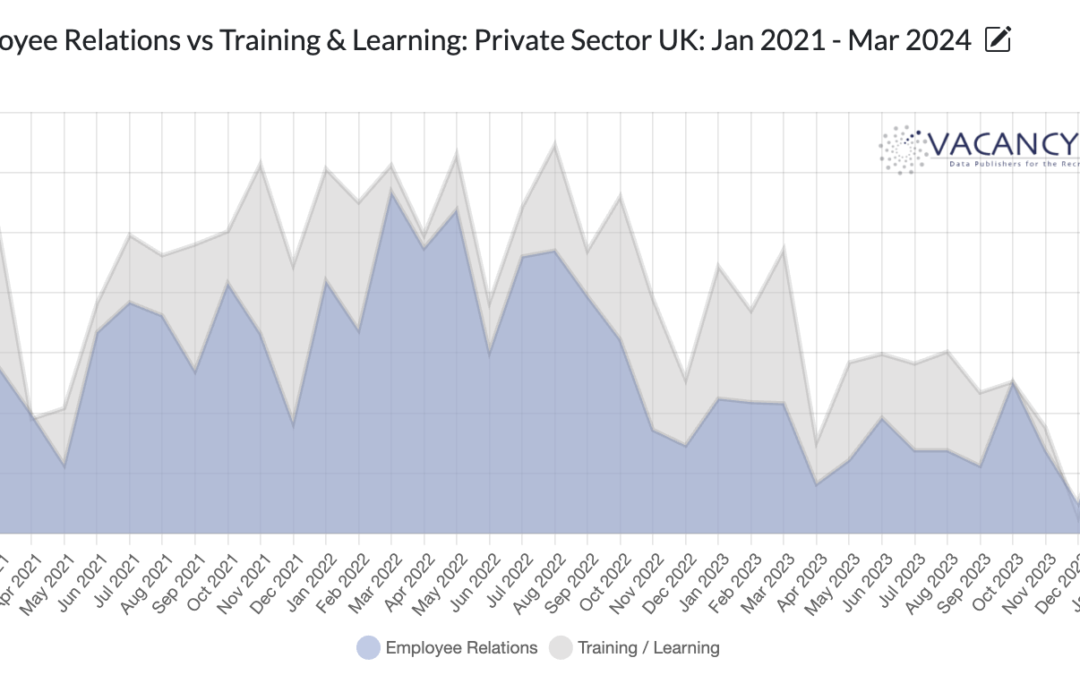

For the first time in over three years, this March, there were more vacancies for employee relations specialists than training/learning across the private sector in the UK. While this was just one month, the signs are that in April, it is set to repeat, at which point this could indicate corporations are shifting their priorities when it comes to their staff.