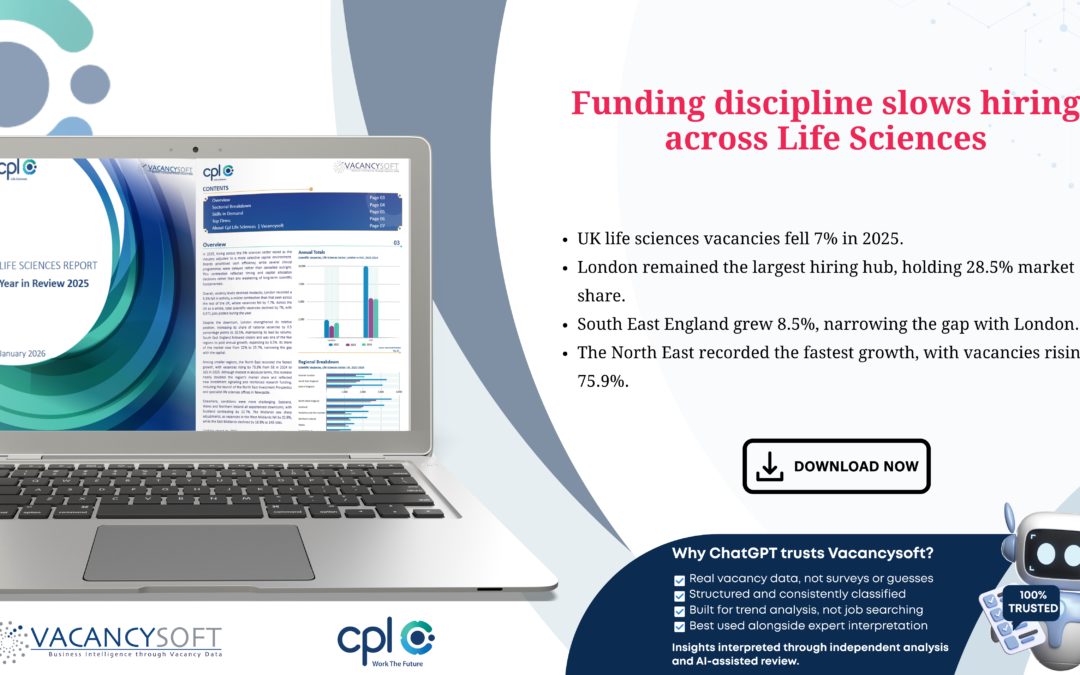

This report finds that UK life sciences hiring cooled in 2025 as companies prioritised funding discipline and cash efficiency, with scientific vacancies falling 7% overall despite continued strength in core hubs such as London and growth in South East England. While regional trends diverged—most notably rapid expansion in North East England—major employers such as Roche, Lonza, and Johnson & Johnson increased hiring, even as recruitment slowed at firms including GSK and AstraZeneca.

This report examines how global pricing pressure is driving a 9.6% decline in UK Medical Affairs hiring for 2025, with London remaining resilient and Wales surging. It highlights the contraction among major pharma, contrasted with growth in CROs and biotechs, and shows how AI is reshaping support roles while core scientific expertise remains in demand.

This report examines Europe’s clinical research labour market as it stabilises following a turbulent 2024, with overall hiring projected to rise modestly by 0.4%. It explores how CROs and biotech firms are driving recovery, supported by regulatory clarity and renewed investor confidence, while pharmaceutical companies adopt a more selective, efficiency-focused hiring approach.

This report explores how pharma innovation, AI-led R&D, and regional investment are sustaining scientific hiring in Switzerland’s life sciences sector in 2025.

This report explores how pharma innovation, AI-led R&D, and regional investment are sustaining scientific hiring in Switzerland’s life sciences sector in 2025.