This report shows UK real estate hiring remained resilient in 2025, with vacancies rising 0.5% nationally despite a 1.3% drop in London, driven by strong demand for sales and infrastructure roles. Regional growth was uneven, with Scotland leading at 14.2%, while housing-focused firms scaled back recruitment amid slower residential markets.

The UK real estate sector is stabilising, with falling inflation, steady interest rates, and rising vacancies.

The first half of 2024 has demonstrated market resilience despite ongoing economic challenges. While sectors like banking and real estate face pressures from new government policies and global uncertainties, strategic adjustments are evident.

As soon as the General Election was called, it became clear that the second half of the year would see a surge in recruitment in House building. Therefore it is not a surprise that vacancies in Real Estate in July hit record levels. Whilst the Conservatives had tried to implement mandatory house building targets under Gove, such was the resistance from their core constituencies, it was soon dropped. For the Labour Party, they have no such constraint, and as a result, have reinstated the target, and increased it.

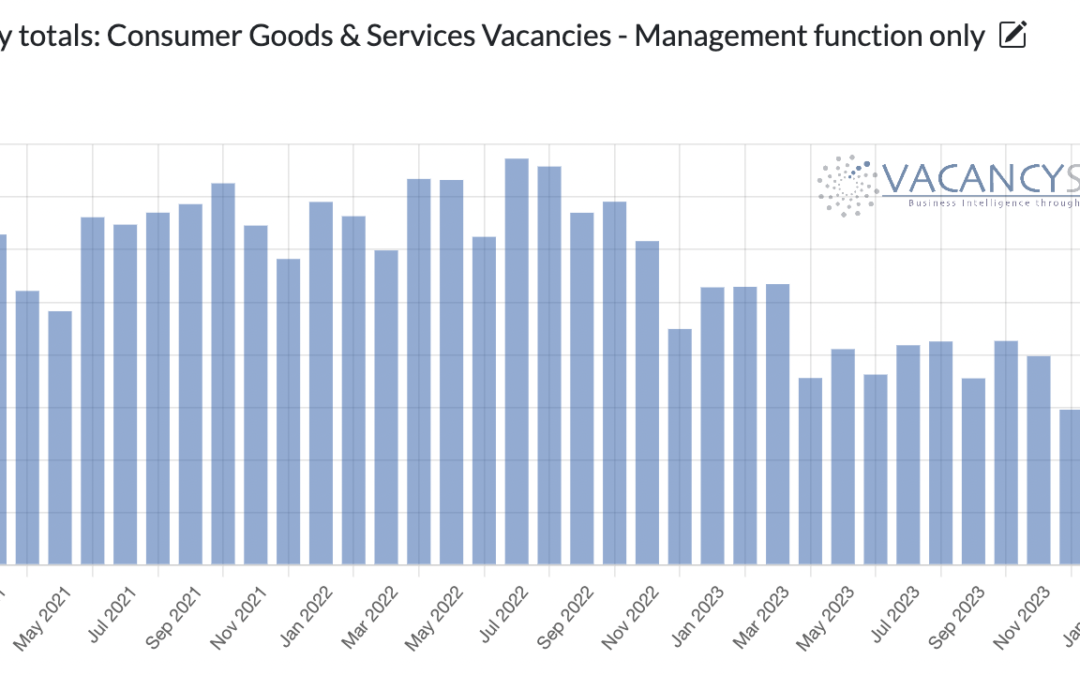

With the clocks changing and the days getting longer, there becomes a tangible shift in the mood of the nation. Typically that translates into a pick-up in activity for retailers. Indeed, Since 2021, the only time that Q2 performed worse than Q1 was last year, equally, that did coincide with the sharp downturn in the economy caused by quantitative tightening, which instantly acted to squeeze the economy.